As the leading global provider of advocate and referral marketing for financial services businesses, we asked our referral scientists in the Buyapowa Labs to identify and break down some of the leading credit union referral programs and highlight what we think they’ve done well and what they could do better.

So our experts grabbed their microscopes, donned their lab coats and took a close look at the following 11 leading credit union referral programs:

What is a credit union referral program?

Let’s start with the basics. A credit union referral program serves as a mechanism to inspire your members to recommend your financial services to their friends, colleagues, and family. The primary objective is to attract new members who can benefit from the services offered by your credit union. Typically, the program offers incentives to an existing member when their referred-in friend opens a new account—be it a checking account, savings account, debit card, or credit card—with the credit union. It can also extend welcome rewards to the newly referred-in account holder upon their account opening, motivating them to engage with their new account.

What are the benefits for running a credit union referral program?

Referral marketing offers a cost-effective strategy for credit unions to expand their customer base and target the right type of new member, particularly given recent research that shows that referred-in customers are not only more valuable than customers acquired from other channels, but also that they are, in turn, more likely to refer new customers themselves. We set out the business case of why referral marketing works with examples of how many large international businesses were built on referrals and we have also explained why referral marketing works so well for credit unions in particular in our analysis of credit union marketing strategies and credit union marketing ideas.

And, in addition, Buyapowa’s own research found that eight out of ten people expect to refer their favorite brands and almost two thirds of all respondents (and almost all Millennials) said they’d view a brand positively or slightly positively if they knew it had a referral program. And only very few people of any age would have a negative or slightly negative perception of a referral program.

How to start a credit union referral program?

If you’re considering a referral program, a good place to start is to audit your customer base and find out how satisfied they are. Credit unions typically have the highest NPS ratings among financial institutions typically averaging +50. This often due to the credit unions ability to offer a personalised service and the proximity to and affinity with the membership and the staff at the credit union. You can audit your customer satisfaction in many different ways from NPS surveys, with exit overlays on the website and with questions from call centre staff and customer service staff on chat or chat bots (‘how satisfied were you with the service today’?), and from in-branch questionnaires, focus groups etc. The main reason ton do this, as well as finding out how to improve your customer service, is to understand the potential you have for referrals. That’s because referral marketing relies on having satisfied customers to act as brand advocates or brand ambassadors. So if you find that you’re member satisfaction is not as high as it should be, then you might want to look at how you can improve that before asking for referrals.

Once you’ve decided that your membership is ripe for referrals, then you need to consider what type of referral program you need and whether you can build in-house or outsource. In almost all cases, we’d recommend outsourcing rather than consuming valuable tech resources building what you can easily buy off the shelf. But we do know of some cases where the credit union has conducted a limited proof of concept built in-house to test the waters before spending more time and money. Although we’d comment that you can often achieve a proof of concept quickly using third party software and because success in referral marketing is often much more than just the software, you can benefit from having the advice of experts who have run dozens of successful referral programs.

Another key decision is to understand the features you’ll need and how sophisticated your referral program needs to be. If you need to ensure that your programs is fully white labelled and on-brand, that you only pay out for confirmed referrals that meet post completion hurdles like using the credit card or making mortgage payments etc., you can offer a choice of rewards and incentives and use gamification to get more referrals, then you would be well advised to speak to the some of the leading enterprise referral marketing platforms. However, if these features are not important to you, then you may be satisfied with a more basic entry level platform, at least to test the potential of referrals.

And finally, as well cost considerations, you’ll need to understand the ability of your tech team and marketing teams to support the set up and running of your program. This should include a full marketing plan to support the ongoing success of your program as we outline here. If you’re talking with an enterprise level provider, your discussions should include the resources needed, timings and best practices for promotion.

Examples of credit union referral programs

To illustrate how effective referral programs can be for credit unions, we have listed 9 examples below with an analysis of what we think they did well and could do better.

But, before we get started, we have to make two disclosures:

Firstly, our research was entirely based on the public-facing pages of these referral programs, and those that don’t require a credit union membership number to login to see the referral program and refer. Where we don’t power the referral program mentioned, we don’t know whether these have been integrated into the back-office systems of the credit unions concerned. And while being able to integrate fully with your back-end systems, to only payout for fully confirmed referrals that meet post-completion conditions, like depositing a specified amount in a savings account or making two loan repayments, or being able to pay out different rewards for customer actions that have different values is a key USP of the Buyapowa platform, we have not discussed this in the study.

And secondly, as alluded to above, we actually power some of the programs mentioned above. Where this is the case, we will mention that. But, as we firmly believe that nobody owns a good idea, if we see someone doing something well we want to praise it, learn from it and implement the best ideas into our own programs.

So, if you don’t already have a referral program for your credit union, then hopefully this article will inspire and convince you to launch one. Whereas, if you already have one, then hopefully the following examples can offer new ideas for you to leverage and make your program even better, or perhaps reach out to a leading provider like us to ask for advice. Let’s begin.

1. Delta Community Credit Union

Introduction:

Delta Community Credit Union, nestled in Atlanta, Georgia, is one of the country’s leading credit unions in the United States with more than $8.5b assets under management and over 430,000 members across Georgia.

Hear from Ollie Moore, AVP, Product & Member Marketing at Delta Community Credit Union about their incredibly successful referral program.

See Full Video

In an effort to drive new member acquisition, Delta launched a digital-first, web-friendly referral program in 2017 that allows members to easily and seamlessly refer friends and family to become members.

Referral rewards:

$50 cash to the referrer (up to 10 referrals per year).

Referee rewards:

$50 cash to the friend when they open a consumer Savings Account with a minimum balance of $5.

What our experts think they got right:

Delta has focused on keeping its referral proposition simple and easy to understand and removes any friction that can get in the way of sharing with a simple sign and by allowing happy members to share in a few clicks by native sharing across email, social media and messaging apps.

Something else Delta has got right is that the rewards and incentives they offer not only create value for both the referrers and referred-in friends but also for Delta as the reward is paying into a Delta account, which encourages the use of the account.

Finally, Delta makes a good job of providing clear instructions and outlining the rules as to what constitutes a successful referral, so referrers know what they have to do to earn a reward.

How would our experts improve their program:

As Delta Community Credit Union is a Buyapowa client, it’s difficult for us to comment here. But like any Buyapowa client, Delta benefits from the advice and best practices we share that we learned from working with over 250 leading brands and retailers worldwide. Delta has chosen to keep its program simple and streamlined and it’s working just great like that. But if at any time they decide that they want to add additional features, like intelligent and tiered rewards, gamification or triggered messages, then Buyapowa will be there to help.

“Our program, we call it ‘evergreen’, it’s one of our bigger contributors toward new customer acquisition. The existing customer and their new referred family of friend, will both receive a cash bonus.”

Ollie Moore, AVP, Product & Member Marketing – Delta Community Credit Union

2. Alliant Credit Union

Introduction:

Alliant Credit Union, headquartered in Chicago, Illinois, is the eighth largest credit union by asset size with more than $12.2b in assets under management and serves over 600,000 members providing savings and checking accounts, credit cards to home, auto and student loans, and beyond.

Referral rewards:

No referral rewards offered.

Referee rewards:

No referrer rewards offered.

What our experts think they got right:

Alliant’s referral program is a very simple program that simply requires a member to submit their details and those of the friend they wish to refer, who will then receive an automated and personalized email from Alliant with an invitation and instructions. Referrers can refer up to five friends at a time.

By allowing a member to invite five friends each time, Alliant’s program does attempt to encourage multiple referrals without much effort.

How would our experts improve their program:

You may have already spotted the obvious improvement opportunity in Alliant’s referral program but let’s dig in. Because the brand has chosen not to offer a referral reward or incentive, its program relies solely on the natural advocacy of its members to drive referrals. However, there is much research into the value of rewards and incentives, and research from Yale found that referral rewards can play a crucial role in overcoming the psychological barriers to referral, while Harvard found that the presence of a friend incentive can actually encourage a member to refer a friend, by giving that friend not only a great recommendation but also a great deal. At least we think Alliant should experiment with exclusive referral rewards that can boost conversion rates and encourage referrers to share and convince referees to join.

While Alliant’s program has a very stripped-down form submission system, it still requires a member to enter the details of their friend and so requires that the member has those details easily available and doesn’t include a typo in an email address etc. This is a typical failing of many old-style referral programs like this, and even a small amount of friction, like having to remember a friend’s email address, could result in a lost referral. Especially when you compare this to the convenience and simplicity of native sharing, allowing you to share in a few clicks without having to enter any personal information. It also relies on the current member actually having the actual or implicit permission to allow Alliant to receive and store their personal details and could result in an unwelcome email being received from the brand, and maybe a spam complaint. Much better, in our opinion, is to have the current member simply send a referral link to the Alliant program and let each referred-in friend decide if he or she wants to give any personal details to the brand.

Another area that could be improved is the reliance on email for the communication to the referred-in friend, when that person, particularly if he or she is in a younger demographic, may prefer to receive messages by chat, Whatsapp or Telegram etc. We think you should use the channel that a referred-in friend is most comfortable with and is most likely to react on, rather than defaulting to email. Additionally, as Alliant sends the message on the members’ behalf, this removes the option for the referrer to craft a personal and more persuasive message.

We think Alliant would also be wise to provide a referral dashboard that lets members log in and see a summary of the progress of their referrals in real-time, whether accepted, declined or pending. The confirmation that a referral is still underway can not only encourage a referrer to give the friend a nudge, it also gives them the confidence that the referral has not been lost, and so may encourage more referrals.

And finally, when it comes to referral, promotion is vital. After all, you could have the best, most generous referral program out there but if you don’t promote it then it’s not going to gain referrers let alone new members. And while Alliant has their refer-a-friend program featured on their website, it is hidden at the bottom, making it difficult to take notice for web visitors. We think that they could also do more to promote the program on social media, to their 33,000 Facebook followers or 6,600 Twitter followers.

3. GreenState Credit Union

Introduction:

GreenState Credit Union is the largest credit union in the State of Iowa and one of the top financial institutions in the United States today, serving not only Iowa but also Illinois, Wisconsin, Nebraska and South Dakota, with more than 350,000 members and more than $5.5b in assets under management.

Referral rewards:

$50 for every friend successfully referred.

Referee rewards:

$50 when they become a member and open a checking account.

What our experts think they got right:

GreenState’s referral program simply requires potential referrers to submit their name and email address before being able to share their referral via email, Facebook and Twitter, or copy and paste a personal referral link. Unlike Alliant above, the program offers $50 for both the referrer and the referred-in friend for each successful referrer. And as the rewards are paid into the bank accounts held with the credit union, this is a great way to ensure that the referral rewards encourage the actual use of the Union’s products.

Clearly, Green State understands the importance of repeat referrals and has not imposed any caps on the number of referrals a particular referrer can make. A typical referral program can get more than 80% of its referrals from less than 20% of all referrers, and provided there’s a robust procedure to verify referrals, you don’t need to restrict the number of referrals any one person can make.

How would our experts improve their program:

We think GreenState would be well advised to provide a referral dashboard that lets members log in and see a summary of the progress of their referrals in real-time, whether accepted, declined or pending. This can reduce the number of calls to customer support to ask ‘what happened to my referral?’ and, by being able to see the progress in real-time, can give a member confidence to refer again, and even give the referred friend a nudge. But also, encouraging referrers to check their referral status in a dashboard also provides the ability to repeat the calls to action to refer and have all the native sharing options easy at hand.

Finally, we think GreenState should experiment with different types of rewards, for example by offering a rewarding choice between, say, cash, Amazon vouchers or cinema tickets. There’s scope to drive even more referrals by using gamification and advanced rewarding features like leaderboards, tiered rewards and short-lived booster campaigns to get members referring again and again.

4. Langley Federal Credit Union

Introduction:

Langley Federal Credit Union (or Langley FCU for short) is one of the top 100 credit unions in the United States with more than $2.8b in assets and over 252,000 members.

Referral rewards:

$30 when their friend becomes a member and opens a new checking account.

Referee rewards:

$30 when they become a member and open a checking account with 10 debit card transactions within the first 60 days.

What our experts think they got right:

As with GreenState above, Langley offers a reward for both the referrer and the referred-in friend, and one that also creates value for the credit union. This is because the rewards are paid into the accounts of the referrer and the new member, which encourages the use of the Union’s products.

As mentioned below, Langley FCU asks the referrer to enter details of the friend so that the credit union can then email the member’s friend on their behalf. We don’t think that this is a great customer experience, as already highlighted in this article, but they do, however, also offer members the option of requesting a personal referral link (via SMS), which they can then share however and wherever they’d like which does go some way to alleviating the issue.

As mentioned above, provided you have robust procedures in place to check that only valid referrals are rewarded, there’s no reason to restrict the number of friends each member can refer. While we can’t comment on whether Langley FCU does in fact integrate its program with its back end systems to check the validity of each referral, it doesn’t cap referrals and even encourages members to refer again and again stating clearly on the program’s landing page that: ‘There’s no limit to how much you can earn.’

Finally, Langley FCU has made the terms and conditions to qualify to be able to refer under their referral program and earn rewards very prominent and clear. This can act to manage customer expectations and avoid disappointment. And Langley FCU has also decided to restrict participation to current members by requiring that referrers enter their unique member number before referring. This is a valid choice for a credit union that wants to ensure that referrals are more credible and targeted by only letting actual members refer. However, the side effect is that it can reduce the number of referrals the program gets, by limiting the number of potential referrers and stopping a potential referral if the referrer doesn’t have his or her membership number to hand.

How would our experts improve their program:

Langley FCU’s interface is perhaps somewhat clunky, and by default requires that a member submit a form with the friend’s details so that the credit union can send a referral message on the referrer’s behalf. As discussed above, this does add some friction as it requires the member to have accurate contact information for the friend readily at hand. It also removes the option for the referrer to craft a personal and more persuasive message, which we think would likely be more convincing than a message from the Union. And finally, the friend might receive an unwelcome email from an unknown financial institution. We think that a far better solution is to offer native sharing by default whereby the member shares a link and personal message with the friend, and the friend decides if he or she wants to come to the credit union and voluntarily share their information.

We understand that Langley FCU doesn’t have a referral dashboard (although, we can’t check for ourselves as we aren’t members), and if that’s the case, we would absolutely advise them to implement a personalized dashboard where members can see the progress of their referrals in real-time and easily access their personal sharing links and buttons. Ideally, these would offer each referrer the choice between typing out a personalized message to their friend or simply using one or more default suggested texts.

As we mentioned above, while Langley FCU’s program doesn’t limit the number of referrals a member can make and specifically draws their attention to that, it doesn’t provide any incentive for those members to actually refer again and again beyond the same basic reward each time. Our advice would be to implement advanced features like tiered rewards, which offer greater rewards based on milestones or stretch targets, like an additional payment when you have successfully referred five new members. Langley FCU could also utilize gamification mechanics like leaderboards, limited-time booster offers and public contests to encourage their members to refer again and again.

Finally, referral doesn’t have to be a blunt tool that offers the same rewards for each and every referral despite the fact that referred-in customers may have a different value to the business based on the type of account they take out and how much they use it. So our experts suggest that Langley FCU has the potential to use intelligent rewards that scale based on the conversion type, such as a new member opening a checking account compared to qualifying and obtaining a loan, and thus the more valuable the new member, the greater the reward they and the referrer receive. It’s a unique upsell opportunity that can persuade a new member to take out that auto loan they’ve been considering or invest in their future with an investment service.

5. Envision Financial

Introduction:

Envision Financial is a division of Canada’s First West Credit Unions serving the Lower Mainland, Fraser Valley and Kitimat in British Columbia, and collectively has more than 250,000 members and C$15.5bn assets under management.

Referrer reward:

The referrer gets C$100 deposited into their account once the friend successfully joins and begins banking.

Referee reward:

Likewise, the friend will receive C$100 once they successfully open a Simply Free Account and complete a recurring pre-authorized debit or credit transaction within 60 days.

What our experts think they got right:

Perhaps the most critical factor for the success of a referral program is promotion, to make sure that members are aware you have a referral program, can find it easily when they look for it and ensure that it surfaces naturally when they have a positive experience with your brand and are minded to refer. Envision Financial does this by prominently featuring their referral program on their homepage, ensuring that all website visitors — in particular their existing members — are aware of the program and encouraged to sign up and get referring every time they visit and log in.

Envision Financial clearly understands the importance of balancing a friction-free and feature-rich referral program with a simple and straightforward signup process where referrers are directed to a personal dashboard which contains the member’s unique sharing links and personalized sharing options that allow referrers to share via email, Facebook, Twitter and even Reddit and Pinterest. And, to make the process even easier, Envision provides the option of default pre-written messages so referrers can get sharing immediately.

By clearly outlining the rules of their program, what qualifies a successful referral, and providing a clear FAQ section, Envision Financial ensures there is no confusion or uncertainty. This manages customer expectations and by having a personalized referrer dashboard, members can see the status of their referrals in real-time, which should reduce the need to call customer support to ask what happened to a referral. All this should increase members’ confidence in referring.

Finally, Envision Financial encourages members to earn up to C$500 in referral rewards each year which, while only allowing each member to make five confirmed referrals in a year, creates framing for the customer encouraging them to think of the maximum they could earn rather than what they will get for just one referral.

How could we improve the First West referral program?

Here’s where we have to admit that Envision Financial, and the other First West Credit Union programs, are powered by Buyapowa. Notwithstanding, we think that the Envision Financial program is a great example of what can be done with the right software and good management. However, as time doesn’t stand still, what’s right today might not be good tomorrow, which is why Envision Financial benefits from the same relentless desire to continue to improve our platform and share best practice advice we have with all our clients.

6. Logix Credit Union

Introduction:

Logix Federal Credit Union, based in Burbank, California, has over 142,000 members and more than $8b in assets under management. The team at Logix FCU have been recognized by Forbes as the “Best In State” credit union for the fourth year in a row, and reportedly more than 96% of their members would happily recommend them to their friends and family and an astonishing 65% of their new business comes via referrals. While their referral program was paused as of June 2023, we can still look at their proposition in detail.

Referral rewards:

$50 when the referred friend obtains a Logix auto loan.

Referee rewards:

$50 when they qualify and obtain a Logix auto loan.

What our experts think they got right:

Logix FCU’s referral program has been focused not on just joining the credit union by taking out any product, but is focused specifically on auto loans. The referral program is streamlined and simple, with native sharing requiring members to only submit their email address to share a pre-written referral message to share via email, Facebook or Twitter.

As is typical in many of the examples highlighted above, Logix FCU offers a reward that is not valuable to both referrers and referees but also to them because paying cash into the member’s account encourages the use of the Logix FCU banking services.

How would our experts improve their program:

While it’s very hard to criticize any referral program that drives almost two-thirds of all new business, it does illustrate that the basis for success in referral marketing is to first ensure that you offer exceptional service to your customers such that you have a large ready pool of potential Brand Ambassadors. And clearly, Logix FCU achieves that based on the statistics shared above.

However, that said, there are still things we think they could improve with their referral program. While they elegantly integrate native sharing to allow members to refer friends in a few clicks, it’s strange that they don’t offer the option of getting a simple link that members can copy and paste into any other channel, such as via SMS or on social platforms like Reddit or messaging apps like WhatsApp and Facebook Messenger. Also by not allowing members the option of crafting their own personal sharing messages, they don’t let them create a more personalized and persuasive copy.

Logix FCU doesn’t require referrers to enter a membership number, which potentially allows even non-members to refer. However, as the referral reward can only be paid into a member’s account, this means that the actions of a non-member won’t be rewarded. We think that the program should better signal that on the face of the program or, alternatively, if Logix FCU is happy for non-members or past members to refer, provided it gets a valid new member as a result, then it could consider offering non-membership based rewards like third-party vouchers, prepaid Visas, etc.

Perhaps the strangest thing is that, given the astounding success of their program, Logix FCU restricts it to only one product: auto loans. Perhaps this is the source of their most valuable members, but if their platform was able to offer intelligent rewards that flex according to the value of the new member acquired, they could reward referrals across their full product range.

And finally, even though the program already generates a huge percentage of new customers, we think that they could even drive more new members if they marketed the program across their website and social media, and linked to it across all customer touchpoints.

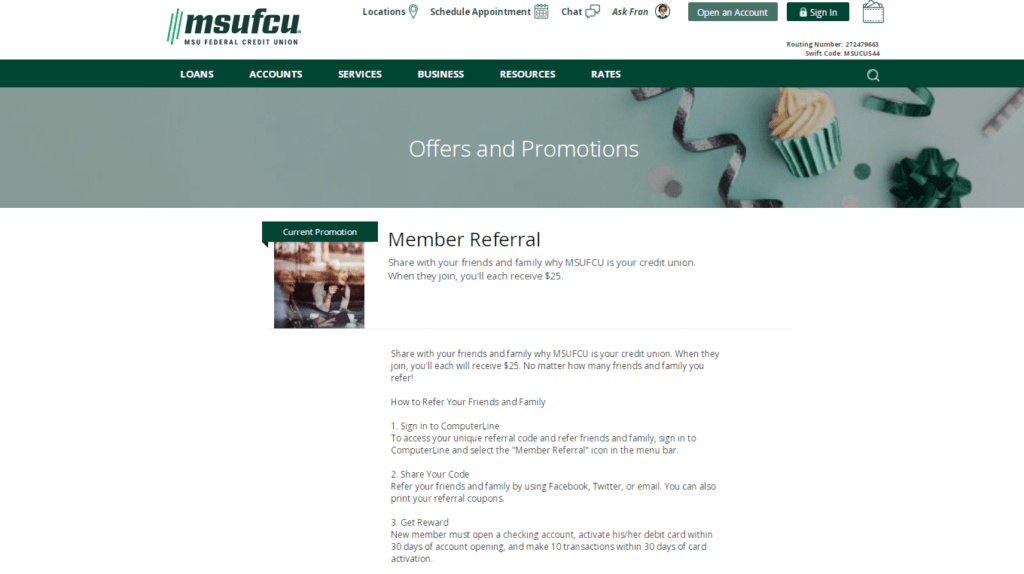

7. MSU Federal Credit Union

Introduction:

Michigan State University Federal Credit Union, or MSUFCU for you acronym lovers, is a popular credit union based in East Lansing, Michigan, with more than 320,000 members and over $6.6bn in assets under management.

Referral rewards:

$25 when their friend becomes a member.

Referee rewards:

$25 when they become a member and open a checking account, activate their debit card and make 10 transactions within 30 days.

What our experts think they got right:

The MSUFCU has been integrated into their banking web app called ComputerLine. Unfortunately, access to the app is limited to members, so we haven’t been to inspect it first hand, but we can see from the program description that members simply need to log in to the app to access their referral code and then share to Facebook, Twitter or via email. There is even the option to print referral coupons.

MSUFCU has clearly outlined the rules of the program and the steps needed in order to complete a successful referral which should manage customer expectations and reduce disappointment. And, as mentioned above, by paying rewards into MSUFCU checking accounts, they provide rewards that are not only attractive for the referrer and the referred-in friend but encourage the use of MSUFCU’s products.

Finally, MSUFCU states that members can refer and earn up to $500 per calendar year, which is the equivalent of twenty successful referrals. While, as we discussed above, as long as the credit union can ensure that only successful referrals are paid out for, it may make sense not to apply a cap. But if you do, MSUFCU encourages repeat referrals by framing emphasizing the maximum amount that can be earned in a calendar year rather than for one referral.

How would our experts improve their program:

Among all the programs listed above, of those that are actually offering a reward, MSUFCU’s referral rewards are the least generous, which suggests that there is scope for them to experiment with their referral rewards, both as to the amount and the type of rewards offered. There are many ways in which they could experiment, either by A/B testing different reward amounts or by running short-term booster campaigns where rewards are increased for a short period of time. We highlighted in this article how the finance brand Revolut constantly changes and offers different mixes of rewards, with each offer set to expire on a fixed date to create a bit of FOMO. Another option could be to offer a choice of rewards to referrers and referred-in friends or to offer different rewards for different product choices.

As mentioned, we haven’t been able to access the ComputerLine app, but we see that MSUFCU states that it can take 4-6 weeks to issue a reward. The reasons for this should be made clear to manage customer expectations, but it may be that the program is integrated with their back-end processing to only issue rewards for validated referrals. If so, that is to be congratulated, but would potentially allow them to offer different rewards according to the value of the referred-in customer. However, if not and this delay is only due to administrative delays, then this is something that could be looked at, as ideally a reward will be paid out as soon as a referral is validated, as delays in rewarding can affect the willingness of a member to refer again.

Without access to the app, we can’t be sure whether they use advanced referral features like tiered rewards or gamification, nor can we see whether referrers are provided with a referral dashboard to provide real-time information on the progress of their referrals. But if not, then these are areas that could be looked at.

8. Wings Financial

Introduction:

Wings Financial is a Minnesota-based credit union that boasts over 329,000 members and manages more than $7.8b in assets. Wing’s Financial’s website features a series of awards that the company has won including Star Tribune’s Best Home Mortgage for 2021, The Balance’s Best Credit Union of 2021 and that it was featured in Star Tribune’s Top 175 Workplaces for 2021.

Referral rewards:

$50 when their friend becomes a member and either opens a Checking Account or obtains a Mortgage Loan.

Referee rewards:

$50 when they become a member and open a Checking Account, and $250 if they obtain a Mortgage Loan.

What our experts think they got right:

Wings Financial offers a simplified and easy-to-use referral program that is perfectly on-brand – which shows that they have understood the importance of having a fully on-brand program to generate trust from referrers and referred-in friends alike.

The program also clearly outlines all important information for referrers, including the basic steps to completing a successful referral, the types of referrals possible and the rewards for each, and a helpful FAQ section. All of which reduces the barriers to referral, increase trust and manage customer expectations.

Wings Financial’s referral program also provides different rewards for different products, paying out a $50 VISA Rewards Card for both parties when a new member joins and opens a Checking account, but this is increased to a $250 VISA Rewards Card for the friend when they qualify for and close on a mortgage. This is an excellent strategy that encourages standard credit union members to join while also targeting higher-value members.

How would our experts improve their program:

While there is plenty to like about Wings Financial’s member referral program, there is still plenty of room for improvement.

Firstly, where and how your referral program is accessed is very important. While the Wings Financial referral program is on-brand, the app that hosts it is not, and when we tried to access it, it struggled to load, and sometimes completely failed to load. As well as ensuring that their app does load quickly, they should be monitoring load times and down service periods to ensure that they don’t turn away potential advocates.

When we were able to access the app, we found that the potential sharing options were limited and required the referring member to enter the friend’s email address so that Wings Financial could send an auto-generated email with instructions. As outlined in some of the examples above, native sharing with the option of typing out a personalized message would likely be so much more effective, as the member would not need to have the friend’s email to hand, a personalized message is likely to be more convincing, the referrer can use the friend’s preferred choice of communication channel and the friend will not get an unwelcome email.

Also, we find it curious that, as a credit union, Wings Financial has chosen to offer a prepaid Visa Rewards Card rather than credit an account with the credit union that would encourage the use of its own products. Perhaps they could offer a choice of rewards, with a higher payment into a Wings Financial account or a lower value as a Visa Rewards card.

Finally, the terms and conditions state that it may take 4-6 weeks to receive a reward, which is quite a long time to wait. This may be due to the fact that they are sending a prepaid Visa Rewards Card. We think that finding rewarding solutions that payout quicker for a validated referral, such as using digital delivery. This should improve member satisfaction and increase the likelihood of repeat referrals.

9. OnPoint Community Credit Union

Introduction:

OnPoint Community Credit Union is a full-service financial institution headquartered in Portland, Oregon. It was founded in 1932 as Portland Teachers Credit Union and has since grown to become one of the largest credit unions in the Pacific Northwest, with over 522,000 members and $10 billion in assets. They introduced their referral program in 2018, and it has received positive feedback from its members. Since its launch, there have been no major changes to the program.

Referrer Rewards:

Members of OnPoint who refer their friends and family to open a new checking or savings account are rewarded with $50 cash. To qualify, the referrer’s friend must also receive a direct deposit of at least $100 into their new account within 60 days of opening.

Referee Rewards:

New members who join OnPoint through the referral program and open a checking or savings account are also entitled to a $50 cash reward. Just like the referrer, they must receive a direct deposit of at least $100 into their new account within 60 days of opening.

What our experts think they got right:

OnPoint’s referral program stands out for its simplicity and transparency. The $50 cash reward for both referrers and referees is substantial and appealing. The program is designed in a way that is easy to understand and participate in, which is crucial for successful referral programs.

How would our experts improve their program:

OnPoint’s referral program leaves some room for improvement:

- Tiered Reward System: Introducing a tiered reward system could provide added motivation for referrers. For instance, offering higher rewards for referring multiple friends and family members or for referring new members who open specific types of accounts could further incentivize participation.

- Streamline the Referral Process: One noticeable area for improvement is the referral form, which appears to be clunky and less user-friendly. To enhance the user experience, it would be beneficial to transition from a complex form to a sleek referral code system. This streamlined approach would provide a more user-friendly experience for both referrers and referees, making the referral process more seamless.

- Revamp the Referral Page Design: The design of the referral page might benefit from a more polished and visually appealing look. Consider redesigning the page to be more slick and modern, with a clear and prominent call to action placed higher on the page. By improving the aesthetics and optimizing the layout, the referral page can become more eye-catching and user-friendly, encouraging more members to participate in the program.

These changes would not only enhance the user experience but also increase the program’s overall effectiveness, making it more attractive and accessible to OnPoint’s members. In sum, the program’s simplicity and rewards are already attractive, and the addition of a few tracking engine and UX updates reward system could make it even more engaging and rewarding for participants.

10. Members 1st Federal Credit Union

Introduction:

As a community-focused financial institution based in Pennsylvania, Members 1st Federal Credit Union launched a referral program in May 2024 aiming to enhance both member acquisition and satisfaction. Known for their dedication to making financial services as accessible and rewarding as possible, Members 1st Federal Credit Union serves its community with a range of personal and business banking services.

Referrer Rewards:

The referrer receives a $25 Amazon eGift Card for every successful referral. This reward is given once the referred friend joins Members 1st and meets the necessary qualifying criteria.

Referee Rewards:

The referred friend also benefits by receiving a $25 Amazon eGift Card upon joining Members 1st and fulfilling the required conditions, such as opening a checking account and setting up direct deposit.

What Our Experts Think They Got Right:

Members 1st Federal Credit Union’s referral program excels in several key areas:

- Dual-Sided Rewards: By offering $25 Amazon eGift Cards to both the referrer and the referred friend, Members 1st ensures that both parties are motivated to participate. This dual-sided approach makes the program more attractive and likely to be shared widely among members.

- Promotion and Visibility: The program is prominently featured on their website and in their communications, ensuring members are aware of the opportunity to refer friends and earn rewards. This high visibility helps in driving program participation.

- User-Friendly Process: The referral process is straightforward, with members easily able to access their unique referral links through the Members 1st online banking platform. This ease of use encourages more members to participate and refer their friends and family.

- Comprehensive Communication: Clear and detailed information about the referral program is provided, including eligibility requirements and how to earn rewards. This transparency helps manage member expectations and reduces potential confusion.

How We Would Improve the Members 1st FCU Program:

Members 1st Federal Credit Union’s referral program is a strong example of how a well-structured and promoted program can effectively engage members and drive new customer acquisition. Buyapowa powers this program and we’re sure to be continuously refining and enhancing the program. We’re here to help Members 1st Federal Credit Union maintain its success and further boost member satisfaction and growth.

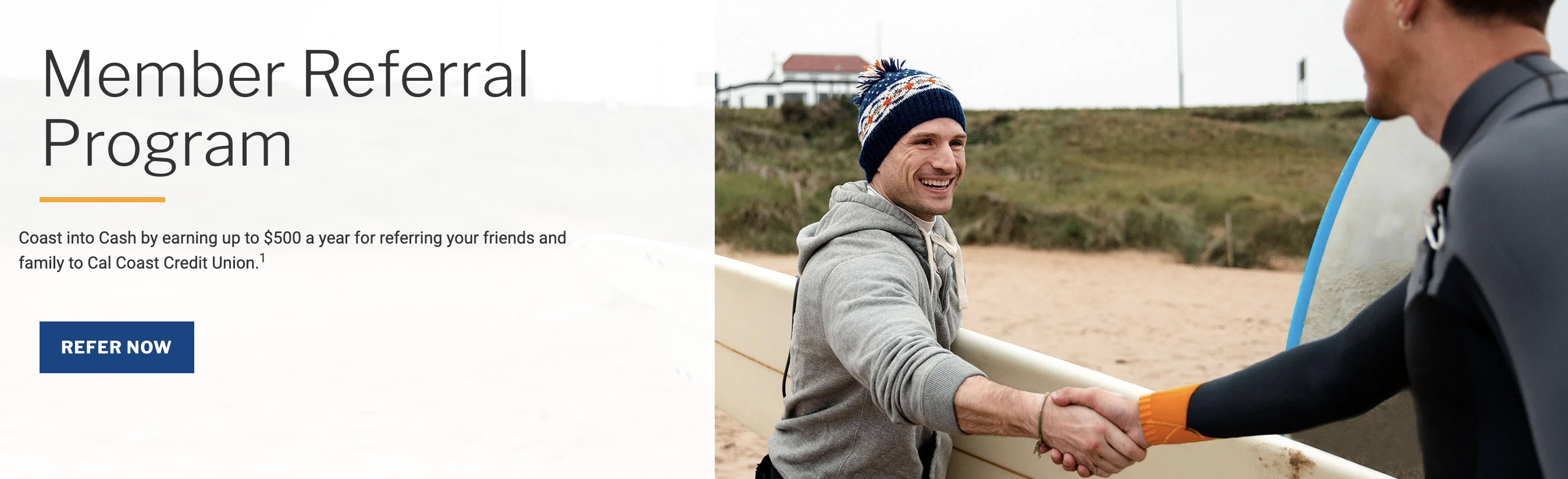

11. California Coast Credit Union

Introduction:

California Coast Credit Union is a prominent financial institution with substantial assets under management and a vast membership base. California Coast Credit Union has become a trusted partner for individuals seeking stability in their banking experience. The powerhouse brand has garnered well-deserved recognition for it’s service, including “Business of the Year in the Financial Services Industry” in 2020 by the San Diego East County Chamber of Commerce. Additionally, in 2018, the credit union’s Chief Information Officer (at the time of the award), Angela Moran, was honored with a Top Tech Exec Award for her forward-thinking leadership in the credit union’s technology strategy.

California Coast Credit Union instituted a robust and user-friendly referral program in June of 2023 to supercharge its customer acquisition and expand its community of satisfied members. This program empowers existing members to share the benefits of California Coast’s financial offerings with friends and family.

Referrer Reward:

California Coast’s referral program implements an intelligent reward structure, offering different rewards depending on the product the new customer takes out. The base rewards are: $50 for a new membership opened, $25 for a New Member Financed Auto Loan referral, and $75 for a new Member Financed Mortgage Loan referral. Rewards can stack but are limited to a maximum of $150 earned on any one referral and a $500 yearly limit on multiple referral rewards.

Referee Reward:

The offering differs depending on the product the new customer takes out. The base rewards are $50 for Open Checking with eStatements and add direct deposit, online banking, or online bill pay. $100 for a New Member Financed Auto Loan referral, and $75 for a new Member Financed Mortgage Loan referral. Rewards can stack but are limited to a maximum of $125 earned through being referred.

What We Like about California Coast Credit Union’s Program:

- Strategic Reward Variation: California Coast’s intelligent reward system, tailoring incentives based on the referred product, showcases a strategic approach. This not only acknowledges the varying value of different products but also encourages referrers to target a broader range of potential members.

- Flexible Reward Stacking: The flexibility of stacking rewards provides an added incentive for referrers to maximize their earnings. With the possibility to earn up to $150 on a single referral and a yearly limit of $500, participants have room for substantial rewards, creating a compelling proposition for active referrers.

How would our experts improve their program:

As California Coast Credit Union is a Buyapowa client, it’s difficult for us to comment here. But like any Buyapowa client, Cal Coast benefits from the advice and best practices we share that we learned from working with over 250 leading brands and retailers worldwide. Rest assured we’re currently working together to keep this program in tip-top shape, based on data-driven insights from our in-house experts.

Conclusion

That’s all for now, but believe us, there is still so much more that we could say on the subject.

While there are many engaging and interesting referral programs being used by credit unions in the US and Canada, there are also just as many opportunities for optimization and improvement to help take them to the next level and turn them into go-to acquisition channels.

So, if you’re interested in supercharging your new member acquisition strategy by launching a referral program or upgrading your existing one, don’t hesitate to reach out to one of our referral experts today. We’d be thrilled to work with you.